This year, the Swiss people voted twice on the future of the pension system. Each time, specific issues were dealt with separately. However, this approach hides the big picture. Is our pension system still adapted to the current times?

Fighting poverty among the elderly before retirement

For many retirees, ageing is no longer associated with the risk of poverty. However, a minority of senior citizens are affected. 92% of new retirees manage to get by after retirement without any additional help from the government. Only 8% receive supplementary benefits when they retire.

However, three-quarters of these recipients already depended on disability insurance or social assistance before retirement. As a result, only 2% of new retirees fall into poverty when retiring. As the authors point out, the best way to combat poverty among the elderly is therefore to increase participation in the labor market before reaching retirement age.

A resilient three-pillar system with room for improvement

Despite economic crises and war in Europe, the three-pillar system has proved successful. As a result, occupational pension benefits have been stable since 2015. However, as careers diversify and life expectancy continues to rise, specific adjustments are necessary:

- Coverage: Reducing the coordination deduction would improve access to occupational benefits, particularly for part-time workers. In addition, the possibility of subsequently filling in the gaps in 3a pillar contributions would enable people who have taken a career break to benefit from better coverage.

- Pension levels: Existing pensions could be improved thanks to a moderate variable bonus. Pension funds could offer the insured a bonus, provided that investment results and the fund’s financial situation allow it.

- Retirement age: A (voluntary) decision to postpone retirement should be considered as an opportunity to secure higher pensions and thus a better situation during retirement. Working longer allows to increase one’s wealth and benefit from it longer. This makes it possible to improve pension levels in all three pillars, without affecting future generations.

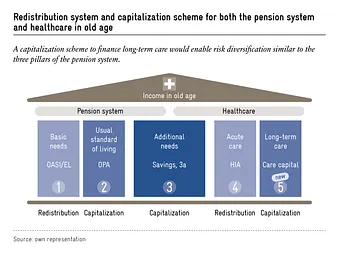

A five-pillar system that takes long-term care into account

Another reason why the Swiss pension system is so successful is that the various pillars are financed differently: the OASI through a redistribution system, occupational pensions and personal savings through a capitalization scheme. We should draw on this positive experience when it comes to financing healthcare costs for the elderly. Today, the rising costs of long-term care are borne primarily by health insurance and increasingly by the public purse. This problem is set to worsen with demographic change. This calls for a new solution that relies more on private provision.

As is the case for pension provision today, we would opt for funding based on a capitalization system. The costs of acute care (e.g. treatment in a doctor’s office or hospital) would be covered by health insurance, as is currently the case. In a more comprehensive pension system, this would be the fourth pillar. Long-term care, on the other hand, would be covered by a fifth pillar, organized in a similar way to occupational pension provision (see figure). Individuals would thus build up a personal care capital that could be inherited. The Swiss pension system would be transformed into a five-pillar scheme.