In its essence, what is banking all about? Many would say it’s the provision of credit. But that is only partly true. Banks don’t just broker money and credit, they also create it – it’s a complex situation. What’s clear, however, is this activity is associated with systemic risk that can lead to bank runs and cause chain reactions in the financial system.

Countries have always tried to keep systemic risk under control. Nonetheless, several bank runs occurred in the USA just over a year ago, and in Switzerland the Credit Suisse was taken over by the UBS using emergency law and federal guarantees. To understand the link between these events we need to take a trip down memory lane.

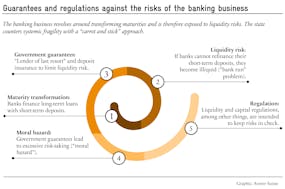

The Land Before Time

The modern banking system has been fragile ever since its beginnings around 300 years ago. Already early on, central banks became “lenders of last resort” to prevent bank runs from happening. Later, deposit insurance was added. Such guarantees are stabilizers, but they come with side effects. They create false incentives such as greater risk taking by banks.

Chain reactions in the financial system must be prevented as a whole. (Adobe Stock)

Various regulations have been put in place to keep these wrong incentives under control. Capital requirements, for example, are intended to ensure that banks take fewer risks and can bear losses from risky activities on their own. The set of rules surrounding the banking system is similar to a carrot (guarantees) and stick (regulation) approach.

This approach worked well before the digital revolution. Back when every financial transaction had to be recorded with pen and paper, the “bank book” was still a real physical book. This was a blessing for regulators, as this technological limitation kept complexity to a minimum and the rules and regulations were straightforward. Digitization changed that.

Digitization as a turning point

Today, digital assets can be moved in just a few clicks and cross institutional and jurisdictional borders within milliseconds. Modern information technologies also enable financial contracts to be combined across countless balance sheets. As a result, the interconnectedness and complexity of the financial system has increased dramatically, reducing the effectiveness of the existing regulatory approach.

Nowadays, the interplay of thousands of financial institutions creates systemic risk. Regulators’ attempts to control individual financial institutions using the old approach have so far only led to one thing: a huge regulatory jungle. As we know, all these rules could not prevent emergency law and federal guarantees from resurfacing a year ago. So, what needs to be done?

A fundamental rethink is needed on an international level when dealing with systemic risk. Chain reactions must be prevented as a whole – for example with a systemic solvency rule. On a national level, an adaptation strategy is also needed. The aim here is to significantly improve the resilience of parts of the financial sector in order to minimize the impact of a systemic crisis on the credit and payment system as well as the monetary order.

The German version of this article was published in “Schaffhauser Nachrichten”.