Revolutionaries appear to have a fondness for Geneva. Around 450 years ago, John Calvin chose the town to settle and set about radically rebuilding the Catholic social order. Now, around a month ago, a certain David Marcus announced that he had chosen Geneva to found the Libra Association, with no lesser aim than to turn the established order of the world’s currencies on its head.

Marcus heads a subsidiary of Facebook called Calibra. He and his team have formulated the concept for a new currency, Libra, and brought the Libra Association into being. Various other corporations are involved in the project besides the US tech giant, including well-known names such as Visa, Vodafone, and Uber. Libra still only exists on paper. But the mere announcement of the new currency has already caused a commotion.

Of course US tech corporations are notorious for grandiose announcements. Some of the promises of salvation offered by the initiators of Libra definitely come from the realms of the most unctuous American PR. Many aspects of the new currency are questionable from a social point of view, and the success of the project is anything but certain. But one thing is clear: if, despite all the obstacles and resistance, Facebook & Co. manage to get Libra off the ground, it will not fail to leave its mark on the financial world.

The reason is the way the new currency project combines a range of different components. Libra isn’t just a payment interface for Facebook products such as WhatsApp – something that Tencent has successfully launched in China with WeChat Pay. Libra isn’t a mere cryptocurrency like Bitcoin or Ethereum either. And it’s not simply a bank that accepts money and provides payment services on this balance. No: Libra brings all these things together to create something new.

1. The various components of Libra

In recent weeks many commentators ranging from monetary theorists and crypto-pioneers to lawyers have examined and described Libra from a specific perspective. While all these experts have identified important points, a partial analysis doesn’t do full justice to the complexity of the project.

Capturing Libra in its entirety means analyzing the interplay of the different elements. The way the project is currently being presented, the focus is on the following five dimensions:

- The technological dimension on the basis of which the new currency functions

- The organizational dimension: how the governance (monetary policy) of the new currency is set up

- The business dimension: the strategy and business model behind Libra

- The macroeconomic dimension: how the new currency is positioned from a monetary

theory perspective - The political and regulatory dimension: how Libra affects existing power and regulatory structures

In the analysis that follows we show that the creators of Libra have made compromises in certain areas to create an advantage in others. Notably this also applies to the business, macroeconomic, and political dimensions – even though many experts have so far focused primarily on one specific conflict of aims, that between technology and decentralized organization. Indeed, Libra is very different from existing cryptocurrencies such as Bitcoin and Ethereum.

Box 1:

What is a blockchain?

A blockchain is an electronic ledger that records entries chronologically and links them in blocks of data. Distributed ledger technology (DLT) enables independent agents to reach consensus on the legitimacy of records without having to resort to a central instance. There are different consensus mechanisms designed to safeguard the integrity of records and prevent them from being manipulated by individual participants (Anthamatten & Lago 2019).

Not a classic cryptocurrency

The media have often presented Libra as a new blockchain currency (see box). That’s only partly true. Various experts have pointed out that the data structure underlying Libra is not a classic blockchain set-up (Lopp 2019; Warski 2019). This fact is emphasized in the Libra white paper: “Unlike previous blockchains, which view the blockchain as a collection of blocks of transactions, the Libra Blockchain is a single data structure that records the history of transactions and states over time.” (Libra White Paper 2019).

How secure and practicable the approach of Libra is will emerge in the coming months. Currently a test network is running with the new protocol, and many crypto-enthusiasts will now be putting Libra through its paces. From a conceptual point of view it’s important to realize that Libra differs from Bitcoin, the best-known blockchain-based currency, in two key respects: consensus and governance.

- Instead of providing proof-of-work by way of processor- and energy-intensive mining, transactions in Libra are first verified by the founding members in a democratic process that runs automatically in the background.

- Some governance processes for the event of upcoming changes to the system are also set down in the Libra protocol: alongside the currency token itself there are also investment tokens which only Libra Association members have that allow them to exercise certain decision-making rights directly (Libra Association 2019).

The advantages of a system like this with a closed circle of operators are lower energy costs and higher capacity. The claim is that from the outset, Libra will be able to process around 1,000 transactions per second. Bitcoin can currently manage 7 to 10 (Anthamatten & Lago 2019), and the Visa network around 24,000 (Tapscott and Tapscott 2016).

The downside of this set-up is that the users of Libra have to take a leap of faith and trust the members of the Libra Association. Unlike Bitcoin, Libra starts out neither open nor resistant to censorship; while it is a form of private digital money, it is not a “classic” cryptocurrency. However, the creators of Libra promise to switch from a closed system to an open, fully decentralized system within five years (Libra White Paper 2019).

They say that the open system they’re working toward will operate on the basis of a proof-of-stake consensus mechanism. The right incentives will be created not through a stake involving costly energy, but through a monetary stake in the relevant currency, in this case Libra. Proof-of-stake entails many, as-yet-unresolved technical and game-theory-related challenges. Ethereum, the world’s second-largest cryptocurrency by market capitalization, has also been trying for some time to switch to a proof-of-stake algorithm – so far unsuccessfully.

Even though not all the technological problems have been resolved, Facebook & Co. are adopting the standard Silicon Valley entrepreneurial approach of simply forging ahead. They’re staking a claim and gathering experience, and if all goes well they’ll have made sure they have a major head start when it comes to customer adoption. On the other hand they’re compromising in terms of trust, especially in the eyes of the crypto-industry.

In Libra’s case the technology on its own is no guarantee the new currency will be used judiciously. Libra is trying to fill this gap in trust by allocating decision rights to different companies organized as an association under Swiss law. To ensure a certain degree of stability in the new currency, Libra is also employing another component used to build trust in the creation of private money: banking.

A bank but not a bank

The association established by the members of Libra is not only a forum for the governance of the new currency. It also provides a link to the physical world. At the start, Libra is to be a currency covered by government securities and national currencies (Libra Reserve 2019). The pool of assets, to be called the Libra Reserve, is the banking component of Libra. A traditional bank also holds various financial assets on the asset side of its balance sheet to be able to offer money-like products on the liability side such as deposits. The creators of Libra hope that this set-up will build confidence in the intrinsic value of Libra and give its price greater stability.

Some have pointed out that the Libra Reserve means that, like a bank, Libra will face the problem of bank runs. But this view falls short, because it fails to take account of the fact that Libra adopts some but not all elements of banking. For instance, it does not engage in traditional fractional reserve banking, but is more comparable with narrow banking.

Narrow banking is a reform proposal for the financial system that takes various forms. It became well-known following the disastrous bank runs before the 1930s Great Depression (Pennacchi 2012). In most cases it requires banks to cover their clients’ deposits with central bank money or government bonds; the Swiss sovereign-money initiative was closely related in spirit with narrow banking. Libra too, at least at the beginning, intends to hold its reserves in secure government bonds and a selection of world currencies.

However, the comparison is only partly accurate, because unlike the deposits of a narrow bank, Libra is de jure separate from a balance sheet. What exactly does that mean? The documents published by Libra so far suggest that for ordinary people, Libra would constitute neither an equity claim nor a credit agreement; Libra’s value for them lies in the fact that it is accepted for payments. Libra only confers entitlement to the underlying securities and currencies in the Libra Reserve to certain predefined authorized resellers. Since a Libra is fungible – in other words like individual Swiss francs, individual Libras are indistinguishable from one another – this structure to a certain extent guarantees the new currency’s liquidity and price stability.

Because Libra is a currency with its own denomination and does not guarantee a fixed exchange rate with other currencies, it can’t break any promise to convert. The extrinsic value is flexible and will fluctuate accordingly, but thanks to the Libra Reserve probably only within a relatively narrow range. That’s a major difference by comparison with money market mutual funds and bank accounts, where there is an (implicit) promise to convert the asset one-for-one (at par) into the currency in which it is denominated. This doesn’t apply to Libra. It’s not a normal stablecoin that tries to replicate an existing currency on a crypto-token.

In this context it’s interesting to note that the creators of Libra might imagine separating their currency from the reserve at some point. This, at least, is how the following passage from the white paper could be read:

“[The Libra] approach is similar to how other currencies were introduced in the past: to help instill trust in a new currency and gain widespread adoption during its infancy, it was guaranteed that a country’s notes could be traded in for real assets, such as gold.” (Libra White Paper 2019)

So ultimately Libra doesn’t have plans to become a new global bank. It actually has the ambitious aspiration of becoming a new global currency. Even though its members are private sector, the project closely resembles a state central bank such as Singapore’s which hedges its currency with a basket of foreign exchange (in the case of Singapore the composition of the basket is kept secret to prevent speculative attacks on the currency). Even if the structure of Libra rules out the possibility of a bank run, the currency naturally doesn’t come without risks. After all, economic history is peppered with examples of both banking and currency crises. And that’s not the only danger that lurks. No wonder diverse regulators have already taken a critical stance.

The Bank for International Settlements (BIS), the Financial Stability Board (FSB), the UK’s FCA financial regulator, and the Bank of England have all commented critically on the launch of Libra (Economist 2019, Financial Times 2019a). Their main concern is systemic risk. According to Mark Carney, the Governor of the Bank of England, stability would be jeopardized once Libra was successful. The Economist magazine (2019) estimates that if every bank account holder in the West switched a tenth of their savings to Libra, the currency could end up being worth more than two trillion dollars on the bond market. This in turn would impact the balance sheets of traditional banks and affect their lending practice – or erode the stability of the financial system because of the banks’ thin capital base.

An economic power not to be underestimated

Apart from this, the international supervisory authorities are also asking whether the entry of large technology companies like Facebook could damage competition in the financial sector. In an advance excerpt from its latest annual report, for example, the BIS explains that tech companies could also build quasi-monopoly structures by using the reach of their existing digital platforms to rapidly achieve economies of scale. This could block competitors from the market and make it harder for new players to enter (BIS 2019).

The BIS anticipates negative welfare effects if this were to happen. A monopoly would allow almost perfect price discrimination, with the creators of Libra able to sting users for the maximum they were willing to pay for a payment infrastructure. According to BIS head of research Hyun Song Shin, this means that aspects of competition policy have to be considered alongside traditional questions of financial stability (Financial Times 2019a).

The fact that regulators are suddenly acting as guardians of financial market competition is already apparent: if Libra manages to get established, there will be consequences for the existing major players in the financial sector. Not one single traditional bank is a founding member of Libra. The degree to which that was a deliberate choice isn’t clear. What is clear, though, is that the new digital payment system could affect the banks. The tech companies are setting about occupying a key customer interface that can be used for diverse financial services.

In a recently published paper, the Association of German Banks (the Swiss Bankers Association’s counterpart in Germany) paints a dark picture of Libra’s implications for established financial institutions, claiming that Libra could result in a loss of client information for banks and further increase pressure on the industry to consolidate. The authors see the main danger if Libra, like the banks, were to be given access to the central bank in the form of an overnight deposit account. In this case, they say, “the comparative advantage of banks would disappear.” They finish their analysis with a prediction: “In the absence of an alternative digital currency supported by banks and governments, Libra’s prospects of success are high.” (Association of German Banks 2019: p.6).

One thing that may well worry established financial institutions is the fact that the founding members are embarking on the project with a large customer base and their war chest full. The BIS’s anti-trust concerns are not unfounded. The figures for Facebook alone, which claims leadership of the project for itself, are impressive. The US company has around 2.4 billion active users worldwide, annual sales just short of USD 17 billion, and market capitalization in excess of USD 550 billion. By way of comparison, the Swiss universal bank UBS, one of the world’s largest wealth managers, has a market cap of a “mere” USD 47 billion (see Table 1).

But the various founder members don’t just bring customers and the associated network effects to the project. They also bring complementary skills. The two payment service providers Visa and Mastercard, and telecom firms Vodafone and Iliad, are ideal partners when it comes to getting the new currency out there. These companies already know the identities of their customers and are thus able to implement regulatory requirements such as know your customer (KYC) and anti-money laundering (AML) more easily.

The two ride-sharing services Uber and Lyft, streaming provider Spotify, and the booking platforms run by Booking Holdings offer services that could be paid for in the new currency on a worldwide basis. With ingoings and outgoings in diverse national currencies, these companies also have a major incentive to support the new global currency. Since both the fees and the exchange rate differences charged are high, there’s considerable potential for savings. This could allow Libra to rapidly acquire new users at international service providers such as Uber and Spotify.

Of course Facebook itself is key to the adoption of Libra. Facebook is an important e-commerce channel for many companies, particularly in emerging and developing countries (Bloomberg 2018). Here the same effect comes into play as for Uber, Lyft, and Spotify. At the same time, Facebook Messenger allows access to everyone, enabling peer-to-peer payments à la Twint in Switzerland and potentially resulting in even more widespread use of Libra.

There has already been an impressive demonstration of how this could work from Tencent in China, whose WeChat has gained dominance of the market for messaging apps by combining social media with e-commerce and payment functionalities (Financial Times 2016). The new possibilities are already a firm feature of everyday life in China: when people meet for the first time they scan their WeChat QR codes; when they buy vegetables at the market they pay with WeChat. Even beggars have now switched to the new payment mode and display a card with their QR code.

Analysts attribute WeChat’s success not only to its user-friendliness and broad functionality, but also to the fact that it was able from the outset to exploit network effects by building on a large number of existing users. This could be an indicator of the Libra’s prospects of future success. After all, Facebook’s WhatsApp is the dominant messaging app in many countries, so network effects are also likely to come into play right from the get-go.

A handful of non-governmental organizations are also on board for the launch of Libra. They give the project humanitarian PR cachet and could facilitate the adoption of the new currency in regions where many people have no or only very expensive access to traditional banking services. There’s particular potential for savings on remittances to developing countries from abroad. According to the World Bank, the average costs worldwide of sending USD 200 were a hefty 7% in the first quarter of 2019 (World Bank 2019).

The launch of Libra therefore placed great emphasis on the provision of cheaper financial services for the poorest people in the world. Of course there’s an element of calculated marketing in all this – but not just that. There are probably also strategic considerations behind the approach. The market for payment services is quite simply less mature in developing countries. That makes it easier to enter the market, and offers quite some business potential in the long term.

In developed countries such as Switzerland, by contrast, demand for Libra is likely to start out relatively small. Financial services in this country work perfectly well, and a new currency isn’t something anyone’s been waiting for. Even so, Swiss financial institutions shouldn’t be lulled into a false sense of security. Once a new, purely digital currency has made the breakthrough in individual niches or developing countries, it’s going to be in a very good position to gain a foothold in the developed world. In the medium term certain revenues from cross-border business are likely to come under pressure, but in the long term there could be a lot more at stake for the banks.

2. You have to consider the big picture

Penetrating areas not yet provided with banking services is likely to be only the first act for Facebook & Co. It’s in the second act that things get really exciting from both a macroeconomic and a political point of view. They way Libra is set up, the new currency can also be seen as a bet on the collapse of the existing financial architecture. Why else would Facebook & Co., in full knowledge of the difficulties, have opted for a new currency with its own denomination?

This approach initially makes the introduction of Libra much more complicated. It would have been easier to bring a dollar or euro stablecoin to market, because the value of both these currencies is already fixed in people’s heads, and no great rethink would have been required, either in developing countries or in the industrialized world. The case of WeChat in China is a particularly good example of how creating a digital replica of an existing national currency is a good way of rapidly reaching the masses.

Sluggish start on the cards

Creating a currency with its own denomination involves overcoming major cognitive obstacles. People have to say goodbye to the familiar status quo, gain trust in the new money, and adjust their inner unit of measurement: paying USD 2.20 in crypto-tokens for a coffee is intuitive, but what about 3.45 Libras for the same thing? Making this kind of change takes time, and means every new currency has big hurdles to surmount.

Libra first has to build and then maintain user confidence in the intrinsic value and stability of the new currency. Given that many people no longer trust Facebook in the wake of all the data scandals, this could be tough going. Added to this, for people to change in the first place the new payment services will have to be easier or cheaper to use. Ultimately it’s a matter of using these advantages to achieve a critical mass of customers so that network effects come into play.

All this is a herculean business task, but if it’s successful a turning point will be reached. At that stage Libra will have made the leap to becoming a currency in its own right. Then, like the central banks in the 20th century, Facebook & Co. could try and gradually decouple their currency from the underlying reserves. In the case of the dollar and the Swiss banks, that involved a slow farewell to precious metals; in the case of Libra it would probably first mean shifting the Libra Reserve into asset classes with higher returns, and later on maybe progressively doing away with these reserves altogether. This way the members of Libra could at some point in the future be reaping the full revenues of money creation, the so-called seigniorage.

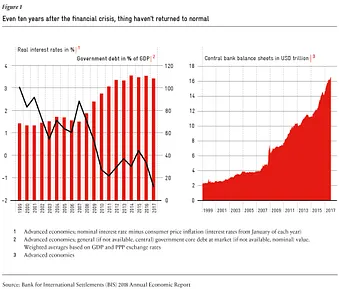

But even more significantly, by proactively shifting the Libra Reserve, Facebook and Co. would be in a good position to face the next financial crisis. After all, the current financial system, based on traditional national currencies, is anything but healthy. Global debt has been mounting unchecked for decades, central bank balance sheets have swollen to dimensions that would previously have been unthinkable, and negative interest rates have long become the norm (see Figure 1). It’s impossible to tell what form the next crisis will take. However, the high volumes of debt and the situation at central banks suggest that the established currencies could also come under pressure the next time around. This in turn could be an opportunity for a private currency, provided it was able to build trust in the run-up to the crisis and set up an efficient and stable payment infrastructure.

The key for private currency projects will be how they prepare for the eventuality of a financial crisis and how dynamic their decisionmaking structures are in a situation similar to 2008. At the same time and as already feared by the international regulators, private currencies are likely to affect the stability of the current system. Depending on how significant private currencies such as Libra become in the next few years, they could either trigger or accelerate a systemic crisis. It’s no wonder that not just regulators, but politicians too, have their antennae out, with no let-up in the criticism even weeks after the announcement of Libra.

Politicians keeping a close eye

Politicians are keeping an eagle eye on Facebook & Co.’s currency project (Bloomberg 2019). Some fear that Libra will put systemically important banks in difficulties and severely restrict governments’ monetary room to maneuver. Financial policymakers in the US are particularly critical. Maxine Waters, chairwoman of the US Committee on Financial Services, claims that Libra threatens national security, poses a cybersecurity risk, and undermines data protection.

The fact that Facebook is presenting itself as the figurehead of Libra is proving to be a serious handicap in the political arena. Sherrod Brown, a Democrat on the Senate Banking Committee, summarily declared that wealth and power had apparently gone to Facebook’s head (Handelsblatt 2019). For many politicians, the main concern at present is data protection. The thrust of their argument is that Facebook has in the past repeatedly treated the protection of the data of their customers with contempt, and that Libra can also be expected to give rise to gross violations of data privacy.

There has also been criticism from Europe, for example from EU parliamentarian Markus Ferber (Bloomberg 2019), who predicts that Facebook could become a shadow bank that circumvents regulations. Meanwhile French finance minister Bruno Le Mair is concerned about national currencies and wants to prevent Libra from competing with the euro or dollar. To this end he is calling for central banks all over the world to look into whether the new Facebook currency might be a gateway for money laundering and terrorist financing (Bloomberg 2019). On this point Facebook has already indicated that it has a technological solution to the issue of anonymity on its blockchain platform up its sleeve, and that identities could be verified (CNN 2019). However, there is tension between these regulatory requirements and calls, also from the regulators, for better protection of privacy.

Besides data protection and system stability, there are also concrete interests at stake for governments in Europe and the US. If Libra were to be a success and its reserve policy were to increasingly move away from the traditional currencies, this could considerably reduce governments’ seigniorage income. There are substantial sums at stake: in Switzerland the Swiss National Bank (SNB) currently distributes a billion francs a year to the Swiss Confederation and the cantons.

Since the dollar continues to serve as the world’s reserve currency, seigniorage is particularly important in the US. Indeed back in the 1960s, the then French finance minister Valéry Giscard d’Estaing even called it an “exorbitant privilege.” It’s hardly a surprise that the present US president Donald Trump recently highlighted the international supremacy of the dollar and declared “We have only one real currency in the USA” (Trump 2019).

3. The significance of Libra for Switzerland

In the whole excitement around Libra, Switzerland also has a role to play. After all, the Libra Association is a Swiss association based in Geneva. In itself, of course, that’s very gratifying for this country. Once more Switzerland can position itself as a progressive, technology-friendly location. On the other hand it is also likely to attract international attention; Libra’s choice of base has already prompted cynical remarks from some politicians in the US.

While the US and the EU currently have enough ways themselves of placing obstacles in Libra’s way, it’s not certain that they will really be able to derail the entire project by these means. It’s possible that Western governments will only succeed in ensuring that Libra won’t initially be available in their countries. But this wouldn’t ward off the long-term risks to the established financial sector. It’s not clear whether this will mean Switzerland comes under political pressure as the home base of the Libra Association.

FINMA is involved

Before Swiss politicians come under pressure, however, Swiss regulators will be in demand. The federal financial market supervisory authority FINMA is already in contact with the managers of Libra. As is customary, however, FINMA will not comment in public on specific providers or licensing procedures. In a hearing before the US Senate Banking Committee, the head of Calibra, David Marcus, confirmed that the Libra Association is to be regulated in Switzerland and supervised by FINMA (Marcus 2019). Marcus will probably request a so-called no-action letter from FINMA. While a no-action letter is not necessary, it does provide a certain degree of legal certainty, which is why many players in the crypto-industry have recently gone down this path.

FINMA will have to assess both the Libra Association and the Libra token. From the point of view of monetary theory it’s a currency with a controlled float and a currency basket, but from a regulatory point of view it poses difficult legal questions. Since Libra has its own denomination that stands in no fixed relation to other currencies, according to FINMA’s classification the currency would actually be counted as a payment token. However, a Libra simultaneously constitutes an (indirect) claim on a currency basket and could therefore also be classified as a foreign exchange derivative.

In this context it will be interesting to see how FINMA will treat the relationship of authorized resellers with the Libra Association. According to Libra documents the plan is apparently for only authorized resellers to interact directly with the Libra Reserve. To this extent authorized resellers are somewhat reminiscent of primary dealers in the US: financial institutions with privileged access to the Federal Reserve. So while for ordinary people a Libra is a payment token without enforceable rights, for authorized resellers it represents a not yet conclusively defined right to a share of the Libra Reserve. This legal quagmire is likely to occupy FINMA for a considerable time to come.

Scenarios for Libra and the SNB

Libra also represents a challenge for the SNB, albeit only if the project enjoys a certain degree of success. This is because if the Libra Reserve at some point also wants to hold Swiss francs, suddenly the SNB will find itself confronted with an important new player on the currency market. If Libra is successful, the Libra Reserve could quickly amount to several hundred billion dollars. By way of comparison, Bitcoin already has a market cap of around USD 200 billion (Coindesk 2019b). As Benoît Coeuré, a member of the Executive Board of the European Central Bank, said recently about Libra, private currency projects of this sort could also impact the transmission mechanisms of monetary policy (Financial Times 2019b).

Depending on whether and to what extent Libra holds Swiss francs as a reserve currency, the SNB could initially profit from higher seigniorage income. In a way this would mean the Libra would digitalize and internationalize the Swiss currency, which would lead to its more widespread use and thus increase seigniorage income. At the same time, however, it would increase the pressure on the SNB in times of crisis. The digital nature of Libra could well make flight into the new currency easier, which would damage the traditional banking sector’s stability and ability to grant credit and, depending on the reserve policy, could also lead to explosive growth in demand for Swiss francs; increasingly, measures to support the financial sector and monetary policy would only work indirectly.

The SNB would face greater challenges if more private currencies were to follow the example of Libra. There’s already speculation as to whether Microsoft, Apple, or Amazon are planning similar projects. Many of the new players on the currency market might then be tempted to back their new currencies with Swiss francs. It’s possible that the franc’s stability would make it attractive and lead to a heavier weighting in currency baskets. Since Libra and its imitators are primarily bought with foreign currency, this would further increase the pressure on the franc to appreciate. The only option remaining to the SNB would probably be a more elaborate regime of negative interest rates or reducing them even more, which would have considerable side-effects for the Swiss economy, including overheating on the real estate market.

4. Looking ahead

More than ten years have passed since the launch of Bitcoin. Mocked by muddled tech-heads as an offhand currency experiment, it’s increasingly turning out to have triggered a wave of innovation. Inspired by Bitcoin and similar endeavors, Libra is probably only the first of multiple projects with the support of powerful corporations in the background that has the potential to influence the global currency landscape. Established financial industry players rightly see the new currencies as a challenge.

So there’s a large possibility that politicians will put a stop to Libra in the next few months. Many reactions from regulators and representatives of the people suggest that the new project can at the very least expect only a sluggish start. But it’s not clear whether this will force the genie back into the bottle.Even if launched only in certain regions, Libra could nevertheless in the long term blossom into a currency that’s used all over the world. Moreover, such big-tech-backed currencies might make it increasingly difficult to prevent technology-driven initiatives in the financial sector.

Challenge for the established financial sector

Just as Calvin was only one religious reformer among many, Libra is only one financial infrastructure project among many. No one can predict what shape the reform of the financial system will take. Alongside private digital currencies such as Libra, classic cryptocurrencies could also gain in importance. Projects such as Ethereum, Tezos, Neo, Eos, Dfinity, and Cardano are pulling out all the stops to resolve the problems of poor scalability and high energy consumption familiar from Bitcoin.

Basically for all these projects a distinction has to be made between the currency and the infrastructure. Based on what we know so far, with Libra these two concepts will coincide. While the new Libra infrastructure allows flows of money to be programmed to a certain degree (by way of smart contracts), at the moment the network seems to be geared exclusively to its own currency, the Libra. This isn’t the case for other decentralized infrastructures. The Ethereum infrastructure, for example, could also be used to issue private or even government currencies that could then be traded globally on the network.

From a macroeconomic perspective, the question of whether a private currency is issued on its own infrastructure or another isn’t completely inconsequential. Much more important, though, is the question of whether the currency turns out to be stable and the underlying infrastructure efficient. If this is the case, it will challenge established financial institutions. The real challenge lies less with the central banks, which after all can issue digital money directly, than with traditional banks that currently play a key role in the payment system by dint of their exclusive access to digital central bank money. This privileged position is likely to be called into question. Once a new payment infrastructure proves itself to be more capable, the traditional bank payment system could come under pressure.

Competition to become the best payment infrastructure might ultimately impact the relationship between the different functions of money. In economic theory, money has a function as a means of payment, as a store of value, and as a unit of account. If the new private currencies were to provide a more efficient way of settling transactions, the payment function of traditional currencies could increasingly be eroded.

This scenario might still seem far-fetched. But in the future payments will be triggered more and more frequently by machines, for example cars that automatically pay fees for road use or emissions. With payments of this sort there could be algorithms in the background going through the ideal means of settling the transaction. It’s easy for machines to calculate with multiple currencies and compare the corresponding transaction costs. In the wake of the Internet of Things, the cognitive hurdle posed by a payment system with its own currency is lower than it used to be.

In certain situations, new currencies could thus assume the function of money as a means of payment. On the other hand government currencies are likely to retain their importance as people’s unit of measurement, if only because taxes and government fees will probably continue to be levied in national currencies. Here there is a powerful network effect at play, because various Western countries have now reached a public sector share of GDP of around 50%.

Perhaps government currencies will also be able to defend their function as a store of purchasing power – “perhaps” because in an increasingly digital world, the function of money as a store of purchasing power could become less important. If the new infrastructures really do lead to a massive reduction in transaction costs, people will probably hold a smaller percentage of their assets as money than they do now. If they need liquidity they can sell assets any time on an automated basis and at low cost. At the same time, non-monetary assets have the advantage of generally yielding a positive return. From the perspective of economic theory the economy would then increasingly resemble neoclassical models, with money becoming a veil.

Support liberalization rather than “libralization”

From a liberal point of view, more intense competition between currencies and the payment infrastructure outlined above are both to be welcomed. The current financial system with its immense raft of regulations and (implicit) government guarantees no longer has much to do with a market, which is precisely why the costs of certain services are so high. Digitalization and decentralization have the potential to boost the dynamic powers of competition in the financial marketplace, to everyone’s benefit.

At the same time, however, a project like Libra backed by tech companies with so much market clout also brings dangers of its own. Besides anti-trust issues,these dangers consist in data protection issues and the emergence of systemic risks. In terms of competition law and data protection, however, the developments we’re seeing at present are a welcome opportunity to clear out some dead wood and formulate the relevant laws even more systematically in technology-neutral terms. When it comes to systemic risks, however, more work is likely to be involved.

The current regulation of systemic risks is too narrowly targeted at specific categories of financial institutions. In recent decades this approach has already shown itself to be lacking. In the run-up to the 2008 financial crisis, for example, there was a massive accumulation of systemic risks despite comprehensive regulation. Since the new payment infrastructures and private currencies should force the pace of disintermediation of old value chains in the financial industry, they’re also likely to accentuate the problems bound up with the institution-based approach that has been adopted so far.

These challenges can’t be ignored, but they should not be allowed to lead to a policy of blocking new financial technologies. Just as the central banks have to circumspectly adapt to the new situation, so too must new ways of regulating systemic risks be found. The launch of Libra should be seen as a wake-up call. There are currently many factors militating against the success of Libra, but even if the project should fail spectacularly, there’s no more stopping the digital transformation of the financial sector. And that’s a good thing, because if new technologies facilitate more efficient settlement of transactions, the result will be welfare gains. It’s a good idea for a small, open economy like Switzerland with a great deal of financial expertise to welcome the changes with open arms – it’s only by accepting change that you can influence the terms of change.

A printed version of this analysis blog including references can be downloaded here as a pdf file.