Notenstein: Methuselah fathered Lamech at the age of 187, and lived a further 782 years. The antediluvian patriarch of the Old Testament thus achieved the record age of 969 years. Calculated in terms of lunar cycles rather than calendar years, this still amounts to 78 years and six months. If that once represented a previously unparalleled lifetime, today there are more and more Methuselahs. This is good news for individuals, but a serious burden for the pension systems of the Western world. To ensure continued fi nanceability, many countries have begun to raise the retirement age. There are already twelve industrial nations with retirement ages of 67 or 68, and more will surely follow suit. Gerhard Schwarz: must we work till we drop?

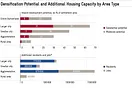

Gerhard Schwarz: The moment to ask this polemical question would have been when state old-age pension systems were first introduced. And then, it would not have been at all polemical; under the first pension system of modern design, implemented by Otto von Bismarck in Germany in 1891, the retirement age was 70 – an age that very few working people actually achieved. When state old-age pensions were introduced in Switzerland, in 1948, men lived on average for 12 years after reaching retirement age (which was set at 65 for both men and women); today the average figure is 19 years. And, as the figure shows, women live for three or four years longer. That means that anyone not struck down by serious illness or an accident may reach 90 or more. Moreover, an increasing number of these 20 years or morecan be enjoyed in good physical condition. Healthcare costs are always highest in the last year of life, regardless of whether people live to an old age or a very old age. Even if the retirement age were raised by three years, people would still be 16 years from “dropping”, rather than 12 years, as would have been the case 50 or 60 years ago.

The idiocy of our system is that it is based on a ridiculous division of life into three parts. First comes the period of education – ever longer and sometimes lasting till 30. Then comes the career, during which people are expected to give their utmost, and work so hard that their health and their marriages are threatened, or actually break down. Then comes the time when they are supposed to enjoy life. It would make much more sense to enjoy life more at an earlier stage, to extend working life considerably in total, but to work somewhat less intensively. That would precisely not be “working till we drop”.

Notenstein: So, living longer means working longer – even if not till we drop. Rather than a general increase in the retirement age, however, you propose a gradual transition to retirement. But that would require greater flexibility in both work and pensions. Individual abilities and needs would have to be taken into account; to that extent, greater flexibility would mean greater individualisation. An international comparison would be of interest here: are there countries that have, through democratic process, made their welfare systems more flexible, and adjusted them to the changed circumstances? Or are the twelve countries mentioned above simply victims of the financial crisis, with no alternative but to raise the retirement age, without any broad acceptance for the measure in the population?

Gerhard Schwarz: You’re right that we can’t apply the same yardstick everywhere. So, I would not go as far as to demand that the state must provide incentives for working longer. It would be quite sufficient to do away with all distortions and put pensions on a proper actuarial basis: those who work for longer get a higher pension, without any tax penalties, and those who retire earlier have to accept a corresponding reduction in their pensions. That would apply for the bulk of the population; of course, there would have to be a separate solution for those unable to work on health grounds. But to your question as to whether the increase in the retirement age in those twelve countries was merely grudgingly accepted because it was practically unavoidable, on account of their empty exchequers. We’re thinking here of countries like Germany, which aims to raise the retirement age to 67 by 2029, in a series of small steps. Here, it seems to me that, because efforts have been made to secure a very accommodating solution for the transitional generation, acceptance is not too bad. Denmark has decided on a somewhat more flexible, «breathing» solution. There, the retirement age is being raised to 67 by 2027, and it will subsequently be adjusted regularly in line with life expectancy. On average, each generation should enjoy their pensions for the same period – 14.5 years. But a much better example seems to me to be what has been achieved in Sweden. There, the retirement guillotine was abolished in 1999. Since then, it has been possible to draw a small pension from the age of 61 (there’s no avoiding the setting of a lower limit), but it is also possible to go on working practically without restriction. Your pension is raised for every further year you work, on a sound actuarial basis. No less important is the option to draw a part-pension from the age of 61; for example to work 60 percent and draw a 40 percent pension. This is very important for a smooth transition into retirement, and the only way to take account of people’s varying situations in life. It may be that we economists have in the past overemphasised that pension reform is dictated by scarce resources; that pension liabilities are simply no longer financeable, however factually correct that might be. For it’s about more than that; it’s about fairness between those who earn about the same amount, but wish to retire at different times. And it’s also about the insight that “one size fits all” applies as little to pension policy as it does to clothes or shoes.

Notenstein: But let’s focus for a minute on the financing problems. The Swiss system is based on promised benefits that must be properly financed, which is not always the case today. For one thing, there are the demographic problems affecting the pay-as-you-go first pillar: the key parameters of the state old-age pension have not changed since its introduction, despite the fact that the relationship between contributors and pensioners has experienced radical change. In 1948 roughly 7 contributors financed one pensioner; today it is 3.5, and by 2050 it will not even be 2.0. The second pillar, financed by capital funding, also has problems, particularly on account of its excessively high conversion rate. This defines the size of the annual pensions that the available capital is converted into at the time of retirement. With a conversion rate of 6.8 percent, a new pensioner with pension assets of one million francs would receive an annual pension for life of 68,000 francs. The problem is that the conversion rate takes insufficient account of the increase in life expectancy since the introduction of the Federal Occupational Retirement, Survivors’ and Disability Pensions Act (BVG). The money paid out to pensioners during their final years by pension funds is thus not the money that they have saved themselves, but the money of younger members of the pension fund, who are still working.

Various popular and parliamentary votes have shown that there is a dilemma in pensions between political practice and actuarial theory. Much that appears politically desirable cannot be financed, and at the same time, measures that would put the pension system on a sound financial basis are impossible politically. How can we resolve this dilemma?

Gerhard Schwarz: What you outline is in reality far more dramatic. For one thing, life expectancy has put a spanner in the works. The conversion rate of 6.8 percent that applies equally for men and women from 2014 is based on life expectancy pre-1990. In the meantime, we now live three years longer. Nor are the financial markets cooperating, as the figure shows. While pension calculations are based on an average annual return of 4 percent, market performance since 2000 has been only 2.9 percent. For this reason, we are redistributing enormous sums – between 600 million and 1.5 billion francs every year, depending on the conversion rate you believe correct – and not from the rich to the needy, but from those now in work to pensioners, regardless of how well-off these pensioners are. We’re talking of sums of up to 50,000 francs per new pensioner. That is the real “pensions robbery”.

Nor should we be under any illusions: these holes cannot be plugged by means of population growth or immigration. The problem is that reform of the BVG is absolutely essential in economic terms, but there continues to be little political chance of it happening. The Swedish model sketched out above seems to me to be particularly successful. But when we realise how hard Switzerland finds even relatively marginal reforms to the pension system, we must accept that this model is not realistic in the short term. A first step would be for the universal pension funds, that combine obligatory cover (the minimum cover required by the BVG for annual salaries up to 84,240 francs) with supplementary cover (beyond the sums saved for obligatory cover) and which include some 85 percent of the insured, to lower the conversion rate on the total pension assets. This is already often being done, so that the effective conversion rate in Switzerland currently averages around 6.5 percent. There would also obviously need to be measures in place to prevent the transitional generation from being disadvantaged by such a reform. Lastly, there needs to be a move in the direction of decentralised decision-making; that is, no prescribed minimum conversion rate for all, but the setting of the rate being left to the individual pension funds. This model too already exists, in Liechtenstein. Legislation on occupational pensions was introduced there five years after the BVG, and a capital error in the Swiss legislation recognised and avoided. The setting of the conversion rate is entirely the responsibility of the boards of trustees of the individual pension funds. This makes it possible to take account of the wide variations in the age structure and financial situation of the pension funds.

Notenstein: Lower conversion rates on total assets in the universal pension funds is at best a makeshift. If the conversion rate for obligatory cover is too high, this simply means that the conversion rate for supplementary cover will be too low. The result is still redistribution, even if a more socially acceptable one, from higher to lower incomes, rather than from young to old. An alternative is the two-fund model; splitting occupational pensions into a basic, obligatory cover and a supplementary management-level cover. What speaks for such a solution is that it prevents redistribution based on a false conversion rate. The legislation offers room for manoeuvre here, and it should be exploited. Pension funds can already offer their members the opportunity to determine their own individual investment strategy, from a given income level and within certain limits. This means that people can select a strategy that best reflects their personal situation and preferences. So, those who wish to counter the overweighting towards bonds of the basic cover can apply a real-asset-oriented strategy for the supplementary part. Also, for two years now, pension funds have been able to set retirement ages flexibly: retirement can be delayed till 70, if employer and employee so wish.

Even if such flexibility is clearly sensible, and very attractive for all those who can take advantage of it, it does not solve the basic, systemic problem. Ultimately, no generation should be able to get rich at the expense of the next one. It is precisely this contract between generations that is increasingly being broken in Switzerland. And what now applies here has long been the case in most of the other industrial nations. Their pension systems are often entirely funded on the pay-as- you-go principle and, due to demographic developments, impossible to finance further without incurring additional large-scale debt. So, if the pension system can no longer be relied on, and there are no signs of correction by the politicians, is it now time for each of us to take matters into our own hands?

Gerhard Schwarz: Fundamentally speaking, self-reliance, and making one’s own provisions, is no bad strategy. It reflects the principles of economic liberalism. To that extent, the third pillar is undoubtedly the most liberal component of the Swiss three-pillar system. Even closer to the principles of economic liberalism is, of course, entirely unconstrained saving, devoid of any tax incentive (or hindrance). Extensive personal provision also makes it much easier to reflect individual preferences. Lastly, the combination of pay-as-you-go and funded schemes, and investment decisions made by the state, pension funds and individuals, offers excellent risk diversification. Which is why I would advise strengthening the third pillar and individual saving, and somewhat reducing the importance of the first and second pillars.

I also find the idea of taking matters into our own hands attractive because the “contract between generations” is largely fictitious. Sadly, there is a good deal of mischief caused with the concept. The pretence is that both sides have signed a contract. It’s a good example of how family-based concepts generally do not translate satisfactorily to society as a whole. Friedrich August von Hayek, who won the Nobel Prize for Economics in 1974, referred to this in his last book, The Fatal Conceit: The Errors of Socialism. While within the family mutual support, love, social expectations and social pressure ensure that parents care for their children, and grandparents for their grandchildren, and vice versa, none of this applies within the anonymity of society as a whole. Why should the young devote an ever-growing part of their income to financing the ever-increasing demands of an older generation resulting from greater life expectancy?Inheritance was also a significant aspect of the old intra-family contract between generations. It sometimes served as a form of pressure, to enforce good conduct and support from children and grandchildren. But generally, it was simply what the older generation could offer the younger generation, as some measure of return for care, support and the financing of their livelihood. Given the then prevailing life expectancy, the heirs generally came into their inheritance in the prime of life, when they could really use it. By 2020, however, some two-thirds of those inheriting will be over 55, and thus already heading for retirement age. So they are effectively twice taken care of: all their lives they have paid their pension contributions, which now bear fruit, and at the same time they benefit from their inheritance.

Notenstein: The topic of inheritance clearly plays a key role in the choice of investment strategy. In discussions with our clients we see that investors who wish to pass their assets on to their children have a much longer investment horizon, and can thus accept greater risk, with correspondingly greater expected returns. If inheritance is made more difficult, as is currently under discussion, the older generation will use up their assets more quickly, and their investments will be considerably more short-term.

But back to the statement that ever-less reliance can be placed on the pension system, so that it is increasingly necessary to take matters into one’s own hands. There are further reasons why this is the case. Pension funds’ investment rules now frequently favour a high bond quota. At a time of zero interest rates and floods of liquidity, however, fixed-interest instruments are no longer risk-free, and offer inadequate yields. Generally speaking, more and more sets of investment rules amount to a minimum quota for (government) bonds. The state thus – and there is no lack of examples of this – ensures a continually satisfactory level of demand for its own debt instruments. At a time of massive state debt, assets locked into a capital-funded system are susceptible to more or less drastic forms of expropriation. In this context, the trend to index-tracking investments also gives us pause for thought, at least as far as bonds are concerned. For here, what index-tracking means is that the most heavily indebted counterparties are highest weighted. For (supposedly) high-quality government bonds, this means that the highly indebted countries of Japan, the USA, the United Kingdom, France and Italy represent 75 percent of the index. Countries offering greater security in terms of debt levels and national deficits, such as Norway, South Korea, Sweden, Australia and Switzerland, by contrast, represent just 4 percent. There is no difference in the real yield from the bonds of the two groups of countries, so investors are not compensated for the risk of investing in high-debt states. Given index-tracking and an overweighting of bonds in pension assets, are not individuals well advised to diversify, and to take countermeasures with their private assets? How do you see this?

Gerhard Schwarz: If you’re looking for investment tips, you’ve come to the wrong address. But I can offer some fundamental considerations. The first is that the time horizon really does play a major role. A long time horizon makes it possible to take losses in one’s stride more easily, or to hang on until the investment recovers. As risk and performance are virtually inseparable, risk capacity is a key aspect for oldage pensions. Accordingly, it makes sense to start as soon as possible. It would be better if mandatory BVG contributions began earlier; say, at 18 not 25. The time horizon also expands when we consider investments beyond our own lifetime. That enables a significantly more aggressive investment strategy. As the success of such a strategy also benefits the subsequent generations in the form of a larger inheritance, consideration should be given to some form of risk-splitting. The young need to offer the old a certain basic security, for only then will the old be prepared to adopt a long-term risk profile.

Secondly, it seems quite clear to me that the corset applied to the pension system is far too tight, and also constricts in the wrong places. It is therefore in the insured’s own best interest to do all they can to ensure that the pension funds get more room for manoeuvre, so that they can take better account of their own, and their clients’ specific situations. Above all, it would be important to finally do away with belief in the security of government bonds, and permit the pension funds broader diversification. Nor should all bonds be lumped together. If broadly enough diversified, corporate bonds are far safer than government bonds. The latter may be continually refinanced in an unparalleled Ponzi scheme, but they increasingly lack substance, a sustainable basis.

Thirdly, given the aberrations in the second pillar, it is important the people save via the third pillar and beyond it. In doing so, it would make sense to correct and compensate for the errors of the closely controlled state sector. Where the regulators of the BVG insist on an irresponsibly high government bond quota, investors should, in their own sphere of influence, focus correspondingly strongly on private companies. Where the obligatory sector relies principally on low-equity vehicles, individual savings should be used to add more risk capital. And where the short-sighted provincialism of state regulations permits only a relatively small share for foreign investments, private assets should be used to take account of globalisation, and of the fact that the growth that will secure pensions over the coming decades is going to occur in Asia, Africa and America, rather than in Switzerland. Fourthly and lastly, as old-fashioned as it may sound, I am convinced that owner-occupied property is among the wisest pension strategies in times of uncertainty and regulatory error. Such an investment generates a secure natural income by way of return, and as long as the owner can remain in the house for the whole of his or her life, it is of little concern what the property’s resale or rental value might be, or how things would have gone had they lived in rented accommodation and invested their money otherwise. The property may generate performance inferior to other investments, but particularly in times of economic uncertainty, of tensions between fears of inflation and deflation, it offers an excellent measure of security of livelihood – a fundamental existential and also emotional necessity.

Notenstein: Gerhard Schwarz, many thanks for a most interesting discussion.

This article was published on www.notenstein.ch, June 2013.