Alfred Escher’s bank is history. A toxic cocktail of private mismanagement, governmental knee-jerk reactions and shaken confidence has taken its toll. The history of scandals and mismanagement at Credit Suisse had long weighed heavily. According to reports, clients and major investors had been divesting themselves of the Swiss bank’s products and securities for months. Following the second and third largest bank failures in history in the US in March, the crisis of confidence dramatically came to a head in recent days.

Way off the Mark in Regulatory Policy Terms

The signs were clear and swift action was required. Last week, the Swiss National Bank (SNB) was the first to step in with liquidity assistance of 50 billion francs. The terms of this measure haven’t been disclosed, but it could be argued that the step was correct from a regulatory point of view, with the SNB fulfilling its mandate as the rescuer of last resort. The same can’t be said of the weekend’s emergency legal maneuver.

Despite all the Federal Council’s pronouncements to the contrary, the takeover of CS by UBS, which became known on Sunday evening, is quite simply a regulatory sin. In the worst case, the federal government and the Swiss National Bank will have to answer for more than 200 billion Swiss francs, more than a quarter of Switzerland’s gross domestic product. Without these state guarantees running into the billions, the takeover of Credit Suisse by UBS would not have come about; the government reinsurance served as the “lubricant” (NZZ).

The media conference kicked off with the Federal Council, the Swiss National Bank and the Financial Market Supervisory Authority (FINMA) explaining the procedure eloquently before the representatives of the banks involved took the floor themselves. Owing to the negative spiral and the imminent reopening of the Asian stock exchanges on Monday morning, everything had to happen quickly; this meant that extensive due diligence was not possible for either the federal government or UBS, the future owner of Credit Suisse. The risk of further expensive surprises in the books will hang like a sword of Damocles over Switzerland’s largest bank.

Well-meaning But Not Well Executed

Credit where credit’s due to the Swiss authorities: the “solution” that’s now been reached was prompted by concerns about the stability of the global financial system. A domino effect had to be avoided. But the chosen procedure, involving a merger of banks organized under emergency law and comprehensive government guarantees, has nothing to do with a liberal order. There will be considerable implications in terms of economic policy.

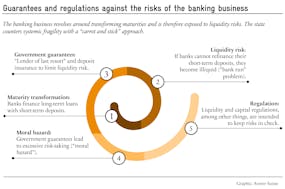

Firstly, from a competition point of view of competition policy, the new “superbank” created by the absorption of Credit Suisse into UBS is an oversized financial colossus. FINMA can overrule possible concerns of the cartel authority under the antitrust rules. But the ones to suffer from a potential restriction of competition will be consumers and companies in Switzerland.

Secondly, the “too big to fail” (TBTF) legislation enacted after a tough political struggle is fizzling out ineffectively. This was developed in the aftermath of the 2008 financial crisis to allow stabilization, restructuring or liquidation in precisely this type of acute case. Implementing these enormously complex rules cost both the authorities and the financial institutions a lot of resources – costs that could apparently have been dispensed with. By applying emergency law, the Federal Council has not only undermined parliamentary participation, but has allowed the TBTF rules to simply degenerate into a farce.

Thirdly, and perhaps most importantly in the long term, the merger of UBS and Credit Suisse under emergency law entails a drastic curtailment of shareholder rights. The future new owners of Credit Suisse, UBS shareholders, were not even consulted about the deal. Legally guaranteed ownership rights in an SMI stock were unceremoniously cancelled. It remains to be seen what the consequences of this breach of the legal certainty for which Switzerland is generally known will be. The loss of confidence is already considerable. Going forward, every (international) investor will have the risk that the Swiss government will curtail shareholder rights in the back of their mind.

A Devastating Political Signal

The end of the liberal order in Switzerland, the land of banks, should actually be a wake-up call for free-market forces in this country. In many quarters the anger, as well as the lack of understanding for the “solution” pushed by the federal government, is palpable. But contrary to expectations, instead of pointing out the extremely problematic aspects from the perspective of the rule of law and freedom, many liberal politicians and business associations are giving the federal government the thumbs-up for its actions of the last few days. This looking the other way won’t work.

The political community is already calling for more influence on the banks and additional regulations – the latter even though the instruments available under the TBTF legislation were not actually properly used. Taking advantage of the banking crisis, political circles that call for more state interventions in general are gaining impetus – even more so because despite billions in government guarantees, CS shareholders have not even lost their entire stake and CS employees are apparently to continue receiving their bonuses – nota bene after an annual loss of 7.3 billion Swiss francs, the biggest since the 2008 financial crisis of 2008.

The takeover of Credit Suisse by UBS, legitimized by emergency law and pushed through with government guarantees worth billions, spells the end of the liberal order in Switzerland’s banking scene. This doesn’t have to be. What’s needed now is an honest reappraisal of the events of the past few days, especially the role of FIMNA and the application of emergency law. What needs to be done to make sure that laws and property rights are not ignored so drastically again in the future? This is essential to restore confidence in a free constitutional democracy.

To safeguard the financial industry in this country, it’s important to remember that it wasn’t the market that failed, but a bank. What’s also needed is greater modesty and humility on the part of the management of financial institutions, as well as a ruthless review of the regulatory framework. Because with the new and even bigger UBS, ultimately the same question will arise as with the now-defunct Credit Suisse: What can be done to make sure the taxpayer isn’t held liable in the event that a large financial institution fails? The liberal order in Switzerland can only be restored if a credible answer to this question is found.