“The pension is no longer enough.” With solemn faces, retirees stared out from campaign posters ahead of last year’s referendum on a 13th monthly pension payment under Switzerland’s state pension system, the AHV. The message was clear: old-age poverty was widespread and worsening.

The emotionally charged campaign worked. Unsurprisingly, support for the measure was strongest among retirees themselves, who stood to benefit directly. But even among voters under 40, more than 45 percent backed the expansion, according to post-election surveys.

Now, as Parliament debates over how to finance the new benefit, another pension expansion is already looming in the form of a proposal backed by the Center Party. The growing burden on Switzerland’s social insurance system will fall primarily on working-age people – in other words, the young. Amid this wave of pension expansion, one fundamental question deserves closer scrutiny: How severe is old-age poverty in Switzerland really? And does it justify such sweeping and expensive measures?

Today, a person in Switzerland is officially considered poor if they have less than CHF 2,400 per month at their disposal. That amount is expected to cover food, housing, and transportation. Health insurance premiums and taxes are not even included, meaning the practical poverty threshold is closer to CHF 3,000.

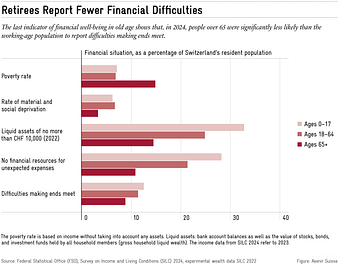

At first glance, the statistics seem to confirm the image of widespread poverty among retirees. Nearly 15%of retiree households are classified as income-poor, compared to 8.4%across the population overall. But this measure tells only part of the story. By focusing solely on income, it ignores a crucial reality: retirees are in a fundamentally different phase of life than working adults. Many draw on substantial wealth accumulated over decades – through private savings, investments and occupational pension funds.

Once wealth is taken into account alongside income, the poverty rate among retiree households is cut in half, falling to 7.3%. And even that likely overstates the problem. Homeownership is not included in these calculations, despite the fact that retirees in Switzerland are more likely than younger people to own their homes. The true rate of old-age poverty is therefore probably even lower.

Measuring poverty, in other words, is more complicated than it first appears.

There is also another way to assess financial well-being: ask people directly how they are doing. Here, too, the results challenge the conventional narrative. Ironically, the very group most often labeled poor in official statistics reports financial hardship least frequently. Compared with working-age adults, retirees are significantly less likely to say they struggle to make ends meet (see chart below).

The same pattern appears in broader measures of well-being. Nearly one in two retirees describes themselves as “very satisfied” with life. Among the population as a whole, only one in three state the same.

The numbers paint a clear picture: retirees in Switzerland are doing comparatively well. Certainly, hardship exists among some older people. But Switzerland already has targeted, needs-based support mechanisms, such as supplementary benefits for pensioners with insufficient means. Helping people who are genuinely poor makes sense. Blanket multibillion-franc payments to an overall well-off generation do not.

The deeper causes of poverty also deserve attention. Poverty usually does not begin in old age; it begins much earlier. People who lose their footing in the labor market often carry that vulnerability into retirement. By the time someone reaches pension age, it is generally too late to rebuild retirement savings. At that stage, targeted support is the only effective remedy.

The best anti-poverty policy, therefore, remains successful integration into the labor market.

That requires a labor market capable of absorbing workers across skill levels and life stages. And such a labor market depends on moderate taxes and social contributions. When payroll taxes and mandatory contributions remain manageable, work continues to pay – both for employees and for employers looking to hire.

Broad pension expansions do little to reduce poverty and may ultimately prove counterproductive. Higher taxes and social contributions make work less attractive, weakening labor market participation and potentially creating the very conditions that can lead to the old-age poverty policymakers claim to fight.

This article originally appeared on May 12, 2026, as a guest commentary in CH Media newspapers, including the Luzerner Zeitung.