Is a single national health insurer the answer to rising health care costs? The idea returns repeatedly in Switzerland’s public debate. Polls suggest that a majority of Swiss support this idea. Many hope that a centralized system would reduce administrative expenses and, in turn, bring down premiums. But that promise is misleading, for three reasons.

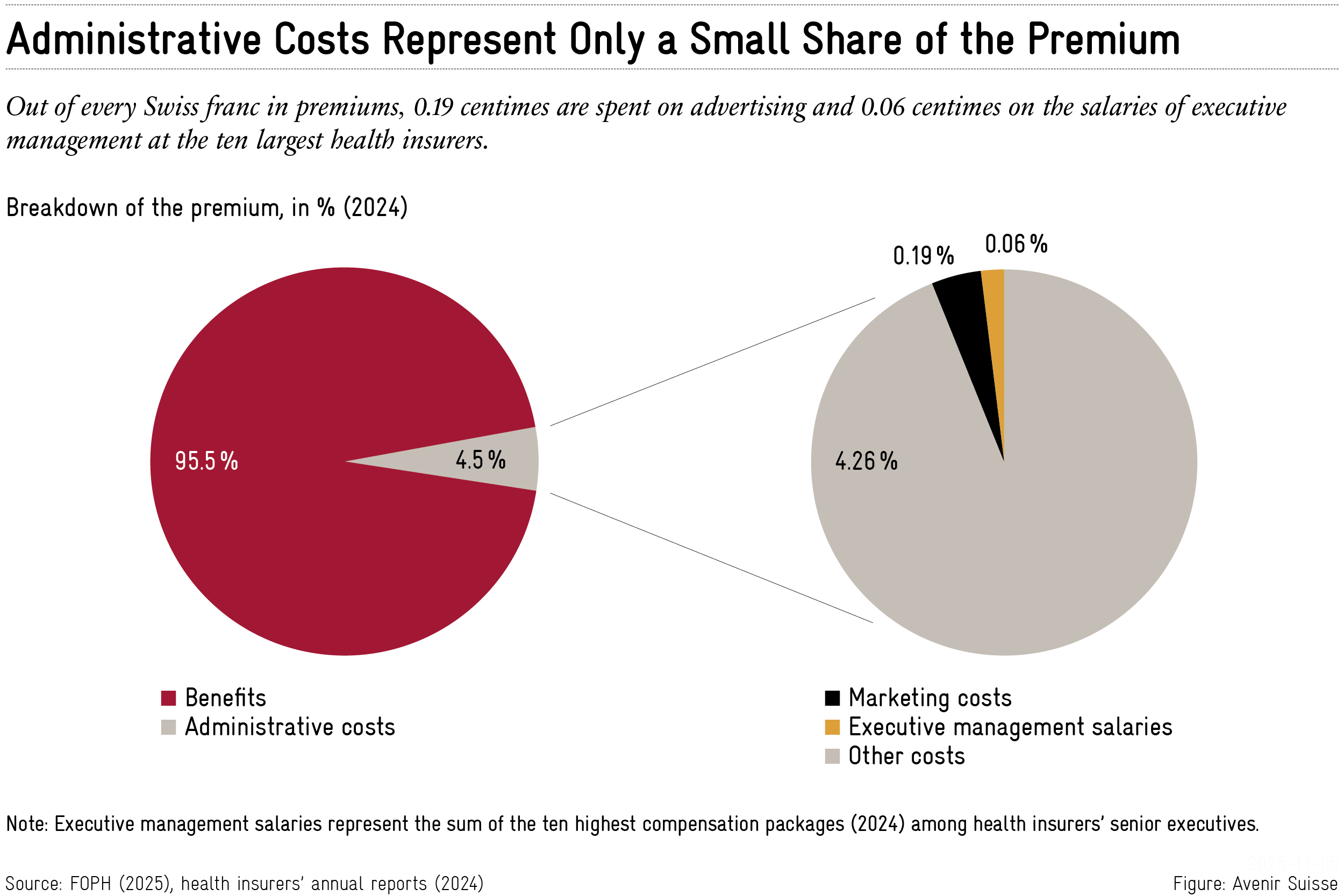

1) Administrative costs make up only a small share of premiums

Critics often point to insurers’ marketing budgets or executive salaries. Health insurers do spend money on advertising to attract customers. Yet the share of marketing costs in the overall premium is tiny. In 2024, out of one Swiss franc in premiums, only 0.19 centimes went to marketing. The same is true of executive compensation: The combined salaries of top management at the ten largest insurers amount to 24.2 million Swiss francs. Whether one considers these salaries excessive or not, they represent just 0.06 centimes per franc in premiums.

Even if a single-payer insurer could cut back on most advertising, personnel and infrastructure costs would remain. And even under the optimistic assumption that a centralized system could reduce administrative costs from 4.5 percent to 2.5 percent, the savings would be modest, especially compared with the expected 4.4 percent increase in premiums in 2026. Moreover, any administrative savings would be a one-time effect, while premiums rise year after year.

2) Competition pushes insurers to be efficient

Critics argue that Switzerland’s current system is overly fragmented, leading to inefficiencies and preventing economies of scale. In reality, competition forces insurers to operate efficiently. Only well-run insurers can offer attractive premiums. That pressure compels them to keep costs under control, for instance by negotiating rates and scrutinizing invoices. In 2016, insurers saved roughly 3 billion francs through such checks – about 10 percent of total premiums – according to the Basel Institute of Economics.

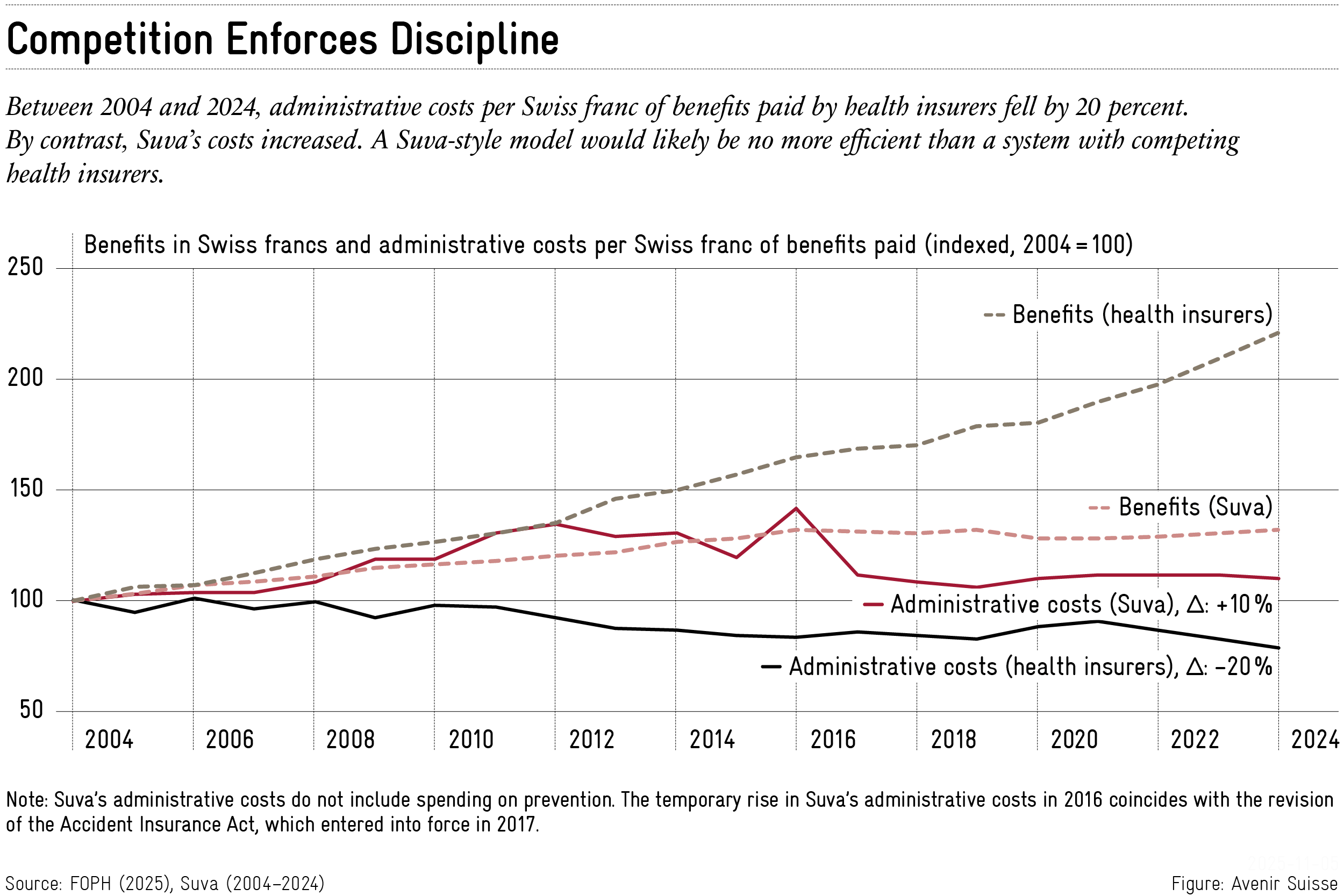

Centralization is no guarantee for more efficiency. Switzerland’s accident insurer Suva, which holds a partial monopoly in its field, is often held up as a model for how health insurance should be run. But the comparison falls short for these reasons:

- First, accident and health insurance cover fundamentally different risks. Accident insurance largely protects the working population against sudden incidents. Health insurance covers illness across an entire lifetime, including age-related conditions. Technological progress, higher levels of education and safer workplaces tend to reduce accident risk. Meanwhile, population aging and the rise of chronic diseases – cancer, diabetes, dementia – push health spending upward.

- Second, the two systems differ in how benefits are paid out. Accident insurance operates on a benefits-in-kind principle: insurers pay providers directly and can exert greater influence on treatments and the development of medical interventions. Health insurance, by contrast, follows a reimbursement model: Insurers pay providers after the fact, once bills have been submitted.

- Third, the trend in administrative costs per Swiss franc of benefits (under the Health Insurance Act, KVG) from 2004 to 2024 shows that health insurers achieved efficiency gains. At Suva however, costs increased. Even if the different types of insurance make strict comparisons difficult, there is no evidence that a “Suva model” with a centralized insurer would be more efficient than competing health insurers.

3) Competition drives innovation

Centralization would eliminate another critical feature of the current system: Its capacity for innovation. All insurers are required to reimburse the same mandatory benefits. But they can distinguish themselves through alternative insurance models.

Many insurers offer plans in which patients must first consult a family doctor, a telephone hotline or a pharmacist before seeing a specialist. Insurers also develop new integrated care models in collaboration with providers and cantons. Examples include the integrated care initiative on Lake Geneva with Ensemble Hospitalier de la Côte and CSS, and the Réseau de l’Arc in the Bernese Jura, supported by an insurer, a hospital group and the canton of Bern. These models improve care, lower costs and lead to lower premiums than the standard plan.

In this way, competition among insurers encourages them to develop innovative products. Insurers have to persuade customers on both quality and price. Nearly 80 percent of people are now enrolled in one of these alternative models. A shift to a single-payer insurer would undermine that dynamism.

Moving from a regulated competitive system to a centralized model would save little money. At the same time, it would remove the competitive pressure that pushes insurers toward efficiency and new products. Anyone serious about tackling rising health care costs should be working to strengthen competition – not weaken it.