The OECD minimum tax was originally intended to ensure that large multinational corporations pay at least 15% tax on their profits worldwide. With a new exemption for U.S. corporations, however, that principle is increasingly being undermined. International tax policy is therefore once again being hotly debated in Switzerland: While some business associations and commentators are calling for Switzerland to adopt the new rules, others are demanding a complete withdrawal — most recently, for example, the Swiss-American Chamber of Commerce, based on a study by the University of St. Gallen.

So, what should Switzerland do? Should it follow suit and adopt the special treatment granted to U.S. corporations? Or is it time to abolish the minimum tax regime altogether? This Q&A sets out the options available to Switzerland — and explains which of them represents the least bad solution.

1. A special carve-out for U.S. corporations: what does this mean?

Under pressure from the United States, 140 countries adopted the “side-by-side” package in early 2026. Since then, the OECD minimum tax has applied to U.S. corporations only to a limited extent. Specifically, the deal distinguishes between two types of minimum taxation:

- Domestic top-up taxes: Each country may continue to top up profits that are taxed too lightly within its own borders to a minimum rate of 15%. This rule continues to apply to all corporations, regardless of where they are headquartered.

Example: A U.S. pharmaceutical company operates a subsidiary in the canton of Lucerne and pays 12% tax on its Swiss profits. Switzerland then levies a top-up tax of 3%, bringing the company up to the required 15%. The side-by-side arrangement does not change this.

- International top-up taxes: Until now, countries applying the OECD minimum tax — such as Switzerland, EU member states, the UK, and Japan — could also impose additional taxation on a corporation’s foreign profits if those profits were taxed too lightly in another country without a minimum tax, such as the United States, China, or India. U.S. corporations are now exempt from precisely this international top-up taxation.

Example: A U.S. pharmaceutical company holds interests in a low-tax country through a Swiss intermediate holding company, with hardly any taxes due there. Until now, Switzerland could also levy a top-up tax on these “undertaxed” foreign profits. For U.S. corporations, this will no longer be the case.

As a result, there are now two minimum tax regimes: one under the OECD and one under the United States. In many cases, the U.S. regime is less stringent: Under the U.S. system, lower-taxed profits in certain countries can be offset against higher-taxed profits elsewhere. In addition, the United States calculates taxable profits according to different rules, which can lead to effective tax burdens of less than 10% in some cases.

2. Should Switzerland claim an exemption modeled on the U.S. approach?

At first glance, it may seem tempting for Switzerland to secure a special carve-out of its own: Swiss corporations could be exempted from international top-up taxes imposed by other countries. Countries such as Brazil and India are currently trying to go down this path.

On closer inspection, however, this option is far less attractive. Following the U.S. example, Switzerland would have to create its own minimum tax regime for domestic and foreign profits. First, this would amount to a fundamental overhaul of the Swiss corporate tax system. Second, under the OECD framework, Switzerland would have to raise its nominal corporate tax rates to 20% — a level that would weaken its attractiveness as a business location. Third, such interventions could backfire if the rules were to change again. Especially in times of global disorder, there is no guarantee for stability.

3. Should Switzerland accept the side-by-side deal for U.S. corporations?

If Switzerland were to refrain from adopting the side-by-side arrangement, it would avoid unequal treatment between U.S. and non-U.S. corporations. At the same time, however, it would expose itself to two considerable risks:

1. Location disadvantages for U.S. intermediate holdings: Many U.S. corporations hold global interests through subsidiaries in Switzerland. If Switzerland were to continue subjecting these intermediate holdings to an international top-up tax, this would create a location disadvantage compared with all relevant competing jurisdictions — both countries without an international top-up tax, such as the United States, China, and India, and countries that have exempted U.S. corporations from such taxation under the side-by-side arrangement, such as EU member states, the UK, Japan, and South Korea.

2. Risk of U.S. countermeasures: The Trump administration has made clear that it is prepared to enforce the special treatment of U.S. corporations politically if necessary — including through “revenge taxes”. This would place an additional burden on the Swiss economy in an already challenging geopolitical environment.

4. Should Switzerland abolish the international top-up tax?

Instead of adopting special rules for U.S. corporations, Switzerland could abolish the existing international top-up tax on foreign profits of subsidiaries altogether. In that case, not only U.S. corporations but all corporations would be exempt. While this may at first appear to ensure equal treatment, it would in fact further disadvantage non-U.S. corporations, including Swiss corporations. There are two main reasons for this:

1. No real tax advantage: Virtually all large non-U.S. corporations operate in at least one country that also enforces the minimum tax internationally — for example in the EU, the UK, Japan, or South Korea. These countries would then capture “undertaxed” profits instead of Switzerland. The tax advantage would therefore not pass from the Swiss treasury to companies, but to foreign tax authorities.

2. More bureaucracy and legal uncertainty: The minimum tax is administratively burdensome: 70% of affected corporations expect annual costs of at least half a million USD. Additional taxation by other countries would likely increase this burden significantly. Affected corporations would be exposed to complex and untested tax procedures abroad. In dispute cases, there would even be a risk of double taxation.

5. Is it time for a complete withdrawal from the OECD minimum tax?

A complete withdrawal would certainly have advantages: Switzerland would instantly become more attractive as a location for U.S. corporations. Not only foreign profits but also profits that U.S. corporations generate directly in Switzerland would no longer be taxed at 15%. This would be beneficial in two ways: First, Switzerland would be on an equal tax footing with countries without an OECD minimum tax, such as the United States, China, and India. Second, it would even gain a tax advantage over countries with a domestic top-up tax, such as the EU, the UK, Japan, South Korea, and Brazil.

Nevertheless, a complete withdrawal would hardly be advisable. As with the abolition of the international top-up tax, under current circumstances it would mean more bureaucracy, more legal uncertainty, and more tax procedures abroad for non-U.S. corporations — without any real tax advantage (see Question 4). In this case, however, additional taxation would affect not only the international top-up tax, but also the domestic top-up tax. For non-U.S. corporations, the consequences would therefore be even less favorable than under a mere abolition of the international top-up tax.

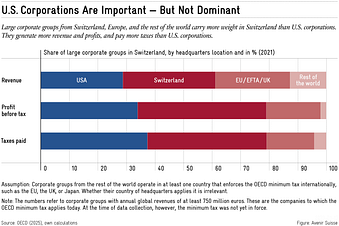

From a broader economic perspective, too, the disadvantages of a complete withdrawal would likely outweigh its benefits. Before the introduction of the OECD minimum tax, corporations from Switzerland, Europe, and the rest of the world were more important for the Swiss economy overall than U.S. corporations. In 2021, they accounted for around 70% of the revenues and profits generated in Switzerland by large corporate groups (see figure). In addition to the global tax rules, the tax environment in the United States has also changed since then. Thanks to the side-by-side arrangement and a major tax reform in the summer of 2025, the United States has become significantly more attractive as a location for large corporations. Initial indications also suggest that more profits are being shifted to the United States. The figures are therefore likely to overstate the future importance of U.S. corporations for Switzerland.

6. Should Switzerland withdraw from the OECD minimum tax while introducing its own top-up tax outside the OECD framework?

The Swiss-American Chamber of Commerce — based on a study by the University of St. Gallen — is calling for Switzerland to withdraw from the OECD minimum tax while at the same time introducing an independent Swiss top-up tax that is not tied to the OECD framework. The idea is that non-U.S. corporations would be protected from additional taxation abroad because their profits in Switzerland would still be taxed at a minimum rate of 15%. Unlike in question 2, Switzerland would not officially seek OECD recognition for a parallel minimum tax regime. Instead, it would create an independent system that continues to subject domestic profits to minimum taxation.

At first glance, the proposal sounds attractive, but it entails uncertainties for Switzerland as a business location. For other countries to accept a Swiss solution, Switzerland would probably still have to align closely with the OECD framework and adopt future rule changes. The more Switzerland diverged from the OECD framework in favor of companies, the greater the risk of additional taxation abroad. Such a “withdrawal” would therefore hardly give Switzerland the hoped-for gain in tax policy autonomy and planning certainty for businesses — and would consequently do little to strengthen its attractiveness as a business location.

There is also a practical problem: The OECD minimum tax could, be abolished immediately. But an independent Swiss top-up tax could hardly be introduced overnight. Until it entered into force, non-U.S. corporations would have no protection against additional taxation by other countries. They would be left exposed for an indefinite period.

Finally, exempting U.S. corporations from an independent Swiss top-up tax would have clear consequences: Under the OECD framework, such an exemption would be considered “discriminatory” and would be sanctioned by non-recognition in countries applying the OECD minimum tax.

Conclusion: Adopting the side-by-side deal is the least bad option

The OECD minimum tax was originally designed as a framework that would be as uniform as possible worldwide. The special U.S. solution has significantly diluted this principle. Switzerland cannot control this development. It can only try to limit the negative effects on its own location.

What is clear is that, under the current international conditions, Switzerland cannot create a tax system that affects all corporations equally, regardless of where they are headquartered. Abolishing the international top-up tax — or even the entire OECD minimum tax regime — would create formal equal treatment domestically. But in interaction with foreign rules, it would further disadvantage non-U.S. corporations relative to U.S. companies, both in tax and administrative terms (see questions 4 and 5). Abolishing the minimum tax would only become an option if the EU fundamentally reconsidered its implementation. That is not currently the case, although it could change in the medium term (see box).

Refraining from adopting the side-by-side deal is no more convincing. This would expose Switzerland to business location disadvantages and unnecessarily increase the risk of U.S. retaliation. The federal and cantonal tax authorities currently appear to take a similar view.

The OECD minimum tax regime, combined with the differing national responses to it, is increasingly creating a confusing web of tax rules and power politics. The growing criticism of the framework is therefore justified and calls for withdrawal are understandable. At present, however, steps such as a non-implementation or a rollback still appear tactically unwise. If geopolitical power relations were to allow Switzerland to withdraw from this increasingly convoluted framework, it should do so as quickly as possible.

Box: The future of the minimum tax in Switzerland depends heavily on the EU

The OECD minimum tax stands or falls with the EU. If the EU were to abandon its implementation, other important countries such as the UK, Japan, and South Korea would likely follow. For now, the side-by-side deal has secured european implementation, as the United States has refrained from retaliatory measures in return. In the medium term, however, this could change: ongoing court cases threaten to invalidate key aspects of the minimum tax in the EU. Politically, too, the minimum tax is not set in stone: As part of the debate on European competitiveness, EU member states could unanimously repeal it.