Switzerland faces costly decisions. After years of underinvestment, the armed forces require billions of francs to restore their defensive capabilities. While the need for action is largely undisputed, the question of how to raise the necessary funds remains open.

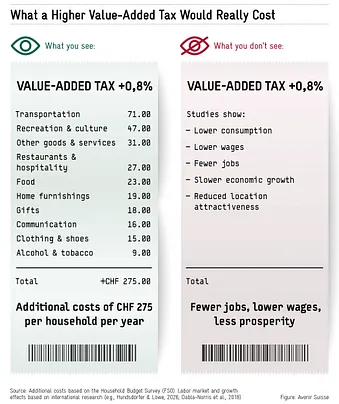

The Federal Council has proposed a temporary increase of 0.8 percentage points in the value-added tax (VAT) rate. The standard rate would rise from 8.1 to 8.9 percent, generating roughly CHF 3 billion annually. What would such a move mean for the economy?

1. The Direct Cost of a VAT Increase

Higher consumption taxes translate into higher prices, eroding household purchasing power. Based on current spending patterns, the increase would cost the average household about CHF 275 per year, according to data from Switzerland’s Household Budget Survey. But that is only part of the story.

2. The Indirect Cost

VAT affects households not only as consumers but also as workers. Businesses often cannot fully pass higher taxes on to customers. In competitive markets, raising prices risks losing demand. As a result, part of the tax burden remains with firms, squeezing profit margins. To offset lower revenues, companies look to cut costs elsewhere — frequently in the most flexible category of spending: labor.

Empirical research covering 27 EU countries illustrates how significant these effects can be. On average, a one-percentage-point increase in VAT reduces wages by nearly 3 percent and employment by more than 1 percent. Small businesses, labor-intensive industries and younger workers are particularly affected.

Applying these findings to Switzerland requires caution. The Swiss labor market, for instance, is more flexible than most of its European counterparts. But the direction of the effect is unlikely to differ. In practice, VAT functions in part as an indirect tax on labor.

Switzerland’s comparatively low VAT rate is therefore a competitive advantage. At 8.1 percent, it is far below the European Union average of more than 21 percent. The lower the consumption tax, the less pressure on wages and employment.

To be sure, all taxes impose economic costs. VAT is generally considered less distortionary than income or corporate taxes. But that relative efficiency does not mean raising VAT is economically neutral.

A model commissioned by the Federal Council underscores the broader macroeconomic implications. It compares two scenarios: a VAT increase and structural spending cuts of equal magnitude. The results are clear. Higher taxes lead to higher prices, reduced consumption, lower employment and weaker growth. International evidence consistently shows that fiscal consolidations achieved through spending restraint are significantly less harmful to long-term growth than those driven by tax hikes.

3. Why a VAT Increase May Not Be Necessary

Since 1990, federal revenues have risen by roughly CHF 40 billion in inflation-adjusted terms — more than CHF 2,500 per capita per year. Most of this increase has gone toward expanding the welfare state. Over the same period, federal spending on the military has fallen by about ChF 500 per capita. The core problem, then, is not revenue but spending priorities.

Several reports point to substantial room for savings. An expert commission led by Serge Gaillard estimated potential fiscal relief at CHF 5 billion annually. Even if fully implemented, however, this would merely slow spending growth rather than reduce overall expenditure.

Further savings appear possible. An analysis by the Institute for Swiss Economic Policy at the University of Lucerne estimates that federal transfers and subsidies amount to nearly 50 billion francs — a complex web that has so far been reviewed only selectively.

There is also a structural challenge. Spending on social insurance and health care has grown faster than the economy for decades, driven largely by demographics. As the baby boomer generation retires, this trend will intensify. Without far-reaching reforms, calls for yet another VAT increase will not be far behind. The ongoing debate over pension financing already offers a preview.

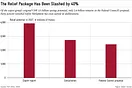

Avenir Suisse has outlined how military funding could be secured over the long term without raising taxes. But such reforms are politically unpopular. Last December, the Council of States significantly scaled back the Federal Council’s proposed spending relief package. Of the original 5 billion francs, just over 2 billion remain. Federal expenditure continues to grow at more than 3 percent per year — and that figure does not yet include additional funds for the military.

Conclusion

The Federal Council’s proposed path — higher taxes — carries both economic and political risks. Empirical evidence shows that tax increases weigh more heavily on wages, employment and growth than adjustments on the spending side. There is also a political hurdle: any VAT increase is subject to a referendum.

If Switzerland aims to strengthen its defense capabilities swiftly and sustainably, the more reliable — and less economically damaging — solution lies on the spending side of the ledger.