The backbone of the Swiss social security system is composed of the first pillar of the Swiss pension scheme – OASI (Old Age Insurance System) – together with the mandatory health insurance. In 2014, both insurances engrossed 44% of the entire social expenditure. Despite the benefits being entrenched in the law and consequently predefined, they are however not pre-financed: it is up to future generations to guarantee them. What does this entail ?

In the OASI, through their wage contributions, working individuals finance the pensions of their contemporary pensioners. The first pillar of the Swiss retirement provision is not based on savings, but on a solidary and well organized allocation system. The ratio of the number of working people to the number of retired individuals plays an essential role : the OASI expenditure will considerably increase in the future as the baby-boom generation retires from the labor market and their life expectancy increases. In order to improve the OASI’s funds – especially in view of the constantly decreasing number of contributors in the future – there are, in theory, three conceivable possibilities.

First of all, the benefits and the annuities can be reduced. However, such cutbacks are particularly difficult to implement on a political level and are also ineffective ; the OASI must guarantee a vital minimum.

Second, proceeds can be raised. In order to finance the augmentation of these costs, without raising the OASI contribution rate, the entire Swiss payroll must equally increase, together with the cumulated wage contributions. In order to achieve this, either more people have to work (e.g., through immigration, through an additional working population who did not work up until now) or the resident population needs to earn more per capita. The problem is that growth cannot be dictated. The situation is different when it comes to increasing the contributions, in order to finance the OASI. The most equitable way to achieve this, while respecting the equity between generations, is VAT : in this case scenario, everyone, young and old, would pay according to their consumption. On the other hand, with higher levies on salaries, Switzerland’s central export economy would be subject to an even greater pressure than it already faces today with the strong franc.

Third, the contribution period can be extended by augmenting the legal retirement age. This has a twofold effect: on the one hand, employers and employees pay contributions to the OASI for a longer period. On the other hand, the period during which the pension is received diminishes. The financial consequences could be significant: increasing the retirement age by 12 months, both for men and women, could enable the OASI accounts to gain approximately 2.7 billion Swiss Francs by 2030. A quick look into the past proves that this can also have a positive effect on the labor market: while women’s retirement age was raised from age 62 to 63 in 2001, and then from age 63 to 64 in 2005, the real retirement age of the concerned cohorts strongly increased.

Still, stretching the retirement age beyond the age of 65 is a political taboo in Switzerland. But if the country does not take these measures, then who should ? Switzerland has one of the highest life expectancies in the world. Its economy is characterized by an advanced service sector and a relatively low working population in sectors with high levels of difficulty, such as agriculture or heavy industry, in comparison to the rest of the world. The situation is different in the majority of industrialized countries : 17 OECD countries have chosen to set retirement age at 67 or 68 years old and have already applied this despite having a lower life expectancy than in Switzerland.

Rising costs in elderly care

Regarding health insurance, supporting health benefits implies an additional burden for the working population in the long run. Health insurance premiums are designed as individual premiums ; therefore, at the outset, there is no interchange between working individuals and pensioners, but only between the healthy and the sick. Nevertheless, given that a large part of health costs occur two years before passing away, primarily in elder people, the individual premium system de facto steers toward a crossed-subsidization from the younger generation to the older generation. The State’s co-financing through tax revenues, of hospitals, care at home services and medical and social care institutions, implies an increasing redistribution of the young towards the elderly. For example, in Zurich nearly three quarters of the income and wealth tax revenue, comes from the population in age of working.

The increase of life expectancy does not have a significant impact on health costs per se ; it merely delays the “costs linked to death”. But with the baby-boomers retiring, the dynamics in healthcare spending are modified : over the next twenty years in Switzerland, the number of people aged 80 and more will increase by more than 80%, while the number of people of working age will only increase by 7%. In the future, if we want to devote as many resources as we do today to the care of the elderly, we will face great financial and organizational challenges.

Constricting cost increase

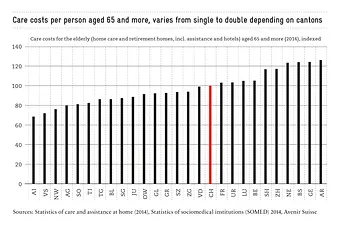

Organizing the care for elderly people is the canton’s responsibility. Federalism allows to take into account the local realities. Nevertheless, we observe considerable differences in relation to the annual care costs per person aged 65 and more. Certain cantons, such as Appenzell Inner-Rhodes, the Valais and Nidwalden, provide care up to 45% cheaper than in the more expensive cantons, such as Appenzell Outer-Rhodes, Geneva and Basel-City – to equal care comparison (see chart below).

A complementary care organization is vital : mild cases could be treated as ambulatory, either at home or in day-care facilities. A stationary treatment, in medical and social care institutions, could be reserved for heavier cases. An “ambulatory and stationary” strategy could be more useful than a simple “preferably stationary” one.

Inspired by the best cantons throughout the health care chain, the potential for optimization is quite substantial. Savings, up to 1.9 billion Swiss Francs, could be realized if the care organization of each canton was as efficient as the national average. This corresponds to 17% of the 11billion Swiss Francs’ expenditure (2014) for the care of the elderly.

Guaranteeing the intergenerational agreement

Despite the potential for optimization, funding the care for elderly people remains a challenge. The Federal Council believes that a 12% increase in taxes will be necessary by 2045 and that the segment of the health insurance premiums, dedicated to the care of elderly people, will double. The long term solution to most of the problems evoked, would be to introduce a mandatory and individual care-deposit in order to pay for the care of the elderly. These savings could be incurred for all care benefits or assistance, that would take place at home or in a medical and social care institution. In case of death, the unused reserves could be bequeathed to the heirs and the support from relatives could thus be honored. This could strengthen the personal responsibility and incentive to save resources.

This care-deposit could also cover the average care cost in an elderly home (excluding accommodation services). This could be achieved through a monthly disbursement of roughly 250 Swiss Francs. At first glance, this could be considered as a relatively high cost. Nevertheless, close to 70% of this amount is financed today through other channels; primarily through tax revenues and health insurance premiums, which could be reduced accordingly. Since the obligation to contribute would only start at 55 years old, the younger covered individuals, as well as their families, would be significantly relieved. If a person were not able to make this payment, the State could support them, in the same way as health insurance premiums are reduced. If the care-deposit were not sufficient, the expenditures could then be covered through private resources or complementary benefits, as is already the case at present. A safety net should be maintained: the State would only intervene in a subsidiary manner, instead of resorting to the “watering can” principle.

Transforming without dismantling

The funding of the OAIS and the long term guarantee to care for elderly people, puts this intergenerational arrangement to the test. In the future, if younger generations “limit themselves” to paying as much as the previous generations, the money will not be enough to enable the elderly to grow old with dignity. Likewise, if the elder generations expect to receive the same financial benefits as those that preceded them, the burden on the working population will no longer be bearable. Therefore, a review, and not a termination, of the intergenerational agreement is necessary. In any case, the commitments when it comes to the benefits that currently prevail, should not be considered to the detriment of the future generations. Under the new 2020 pension scheme, the 70 Swiss Franc extension will cost the working population an additional 1.4 billion Swiss Francs each year; this is the exact opposite course we want to take.